Under a DDP Incoterm, the seller provides literally door-to-door delivery, including customs clearance in the port of export and the port of destination. Thus the seller bears the entire risk of loss until goods are delivered to the buyer’s premises.

A DDP transaction will read “DDP named place of destination.” For example, assuming goods imported through Baltimore are delivered to Silver Spring, the Incoterm would read “DDP, Silver Spring.”

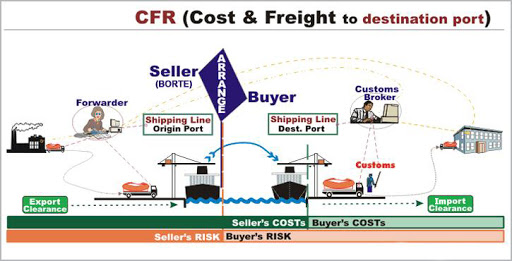

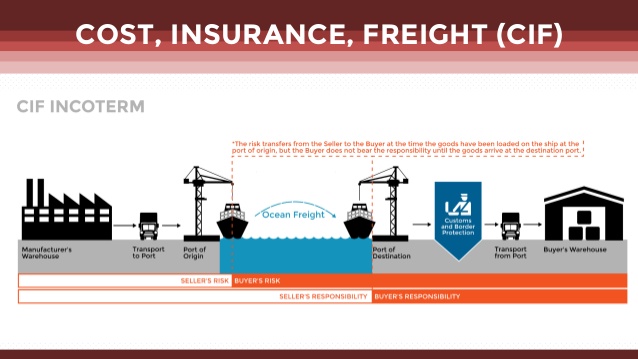

If CIF is the customs valuation basis, the costs of unloading the vessel, clearing customs, and delivery to the buyer’s premises in the country of destination—including inland insurance—must be deducted to arrive at the CIF value.

Rules of the Road

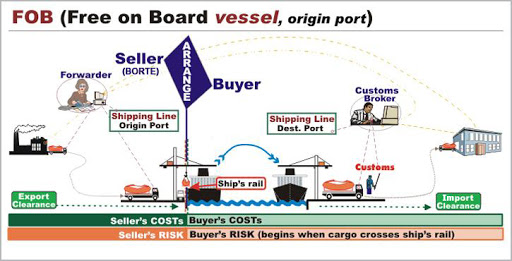

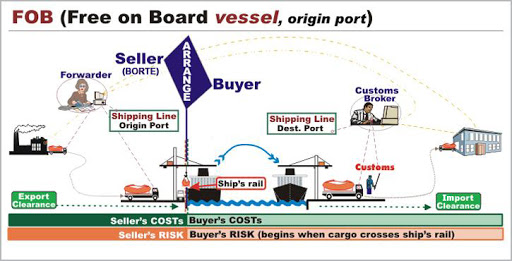

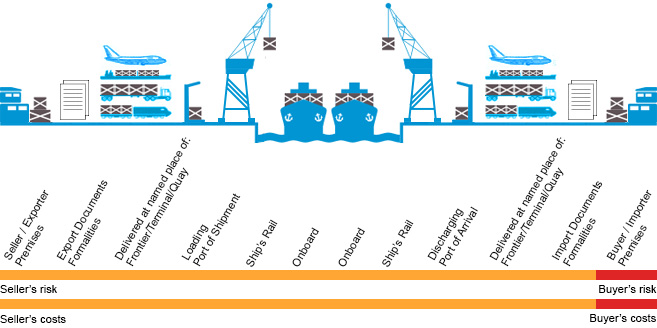

A)It is the seller’s primary duty to deliver the goods on board the vessel named by the buyer at the named port of shipment on the date or within the period stipulated and in “the manner customary at the port.” The parties in these circumstances have to follow the custom of the port regarding the actual measures to be taken in delivering the goods onboard. Usually the task is performed by stevedoring companies, and the practical problem normally lies in deciding who should bear the costs of their services.

B)A special agreement has to be made to establish who is responsible for “trimming” or “lashing and securing.”

C)A special agreement has to be made to establish who actually pays import duty and/or other import taxes.